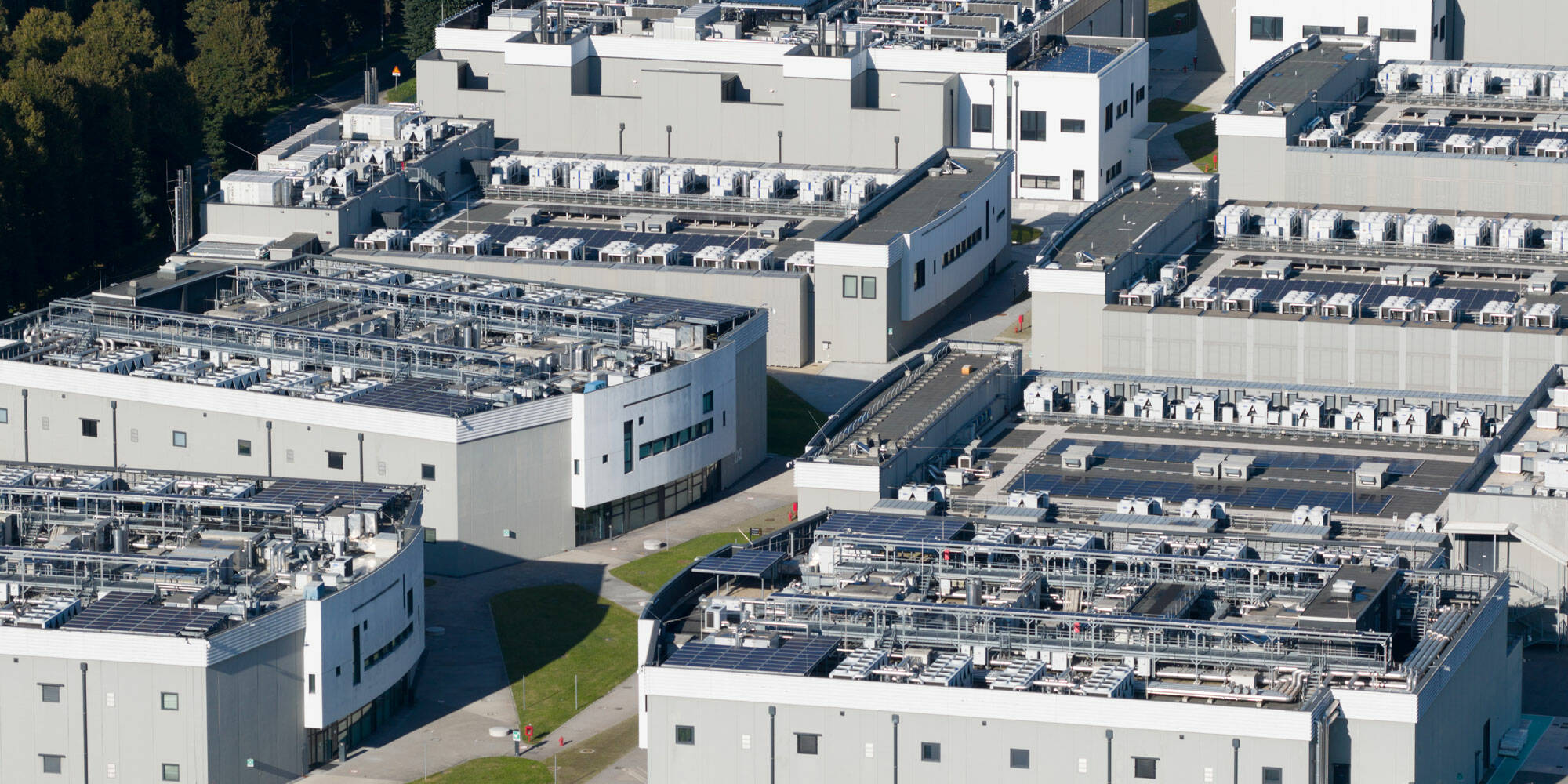

NIMBY pushback begins to bite US datacenter buildout

New datacenter capacity under construction in primary US markets declined in the second half of 2025, as community opposition increasingly disrupted planning approvals - a dynamic commercial real estate firm CBRE says is reshaping the industry.

According to CBRE's North America Data Center Trends H2 2025 report, this is the first time since 2020 that the primary-market pipeline shrank, ending last year at 5,994.4 MW, down from 6,350.1 MW at the close of 2024. The drop comes despite surging demand for compute power to support AI development.

As a result, the overall vacancy rate – the proportion of capacity available in those primary markets – fell to a record low of 1.4 percent, even though CBRE reports that supply increased by 36 percent year-on-year to 9,432 MW.

Average monthly rental rates for a 250 to 500-kilowatt (kW) requirement also rose by 6.5 percent to $195.94 per kW/month, representing the fourth consecutive annual increase.

Rental rates continue to bounce due to the limited availability of powered land and capacity constraints in key markets. CBRE forecasts rent growth to continue outpacing inflation for the next two to five years.

Community involvement is a trend to watch - a key factor in permitting and zoning approvals. In markets like Loudoun County, Virginia, where there is a high concentration of server farms, public sentiment and workforce impacts are having repercussions for development timelines.

Local opposition is a growing issue that datacenter developers face. It was a hot topic of discussion at the Datacloud Global Congress in France last year. Communities fear the effect that facilities might have on energy prices, water supplies, and the environment through noise and pollution from generators.

Projects in the US face lengthy delays and even cancellations amid growing grassroots opposition across the states.

In response, zoning requirements may mandate the inclusion of green spaces or barriers to reduce visual and noise pollution. Authorities may also impose noise regulations to limit disturbance and protect quality of life for nearby residents.

CBRE notes that at least 36 US states now offer targeted incentives for datacenter developers. These include tax exemptions and abatements, which are becoming significant factors in site selection as states dream of AI-driven growth.

This is also a bone of contention for communities, with nonprofit Good Jobs First highlighting last year that taxpayers are kept in the dark about the incentives on offer, while states that calculate their returns find they are losing money on the deals.

Other trends listed by CBRE include on-site power generation becoming routine in large-scale datacenter planning, and the shift from AI training to inference workloads driving demand for more regional, distributed facilities closer to end users. That pull is reshaping site strategy and accelerating growth in previously overlooked secondary markets.

CBRE says vacancy rates are likely to remain at all-time lows for the near future due to limited new supply. It does not expect the number of datacenters under construction to increase much this year, with projects stalled at the planning stage due to permitting, zoning, and power procurement challenges. ®