Forget AMD: 4 AI Stocks That Could Beat the Crowd

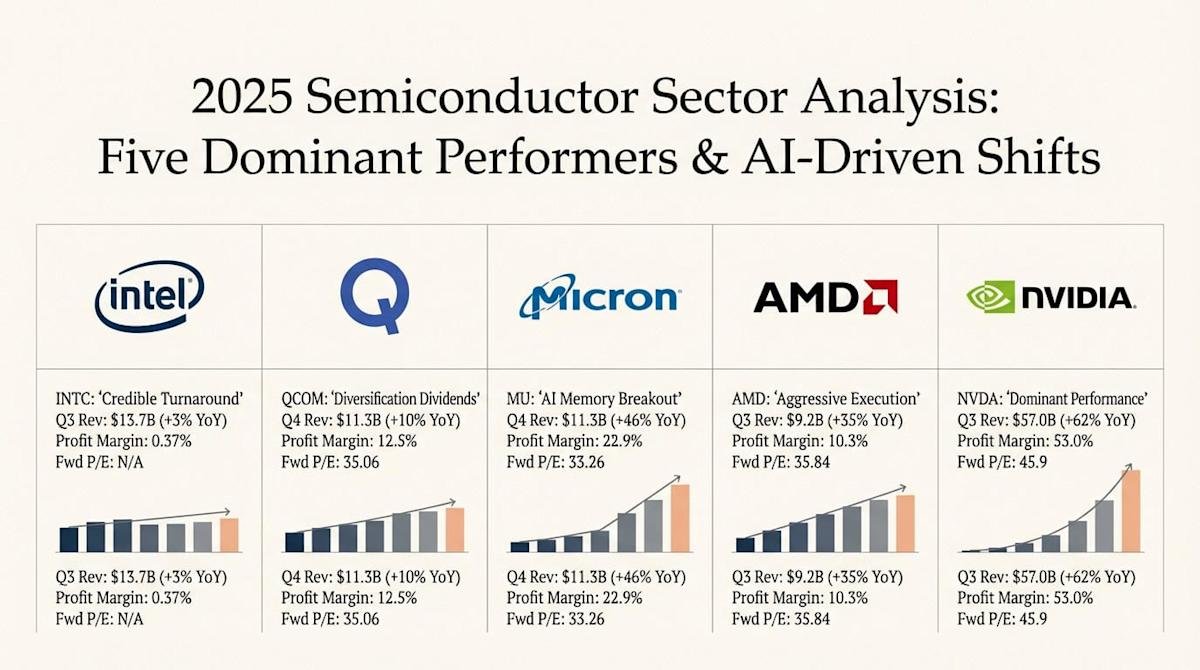

Quick Read Advanced Micro Devices (AMD) as the “NVIDIA alternative” is now a crowded consensus trade that ignores CUDA’s deep moat and custom silicon trends. Micron Technology (MU) collects mandatory AI infrastructure revenue across every advanced accelerator, with fiscal Q1 showing 56.6% YoY growth and order books stretching to 2027. The analyst who called NVIDIA in 2010 just named his top 10 stocks and ASML wasn't one of them. Get them here FREE. Advanced Micro Devices (NASDAQ:AMD) keeps grabbing headlines as the consensus "NVDA alternative" in AI GPUs, the trade every retail account and hedge fund analyst seems to be piling into at the same time. But here's what you should actually be watching. The AMD-as-Nvidia-alternative thesis is the most crowded second-derivative trade in semiconductors. CUDA's software moat is a decade deep, hyperscalers are designing their own custom silicon to bypass merchant GPUs entirely, and every fund manager already owns the name. AMD here represents yesterday's contrarian call after it has gone fully consensus. The real money in this AI buildout flows to the picks-and-shovels suppliers and design partners who get paid regardless of which GPU vendor wins the next benchmark cycle. A few names stand out, and none require you to handicap a duopoly. The analyst who called NVIDIA in 2010 just named his top 10 stocks and ASML wasn't one of them. Get them here FREE. The Memory Layer Is Eating the AI Stack Micron Technology (NASDAQ:MU) delivered fiscal Q1 revenue of $13.64 billion, up 56.6% year over year, with non-GAAP EPS of $4.78 against a $3.94 consensus. Cloud Memory revenue nearly doubled to $5.28 billion at 66% gross margins, and management guided next quarter to $18.70 billion in revenue with $8.42 EPS. Order books reportedly stretch into 2027. Every advanced accelerator on the market requires HBM, and Micron is the only U.S.-based memory manufacturer. CEO Sanjay Mehrotra calls the company an "essential AI enabler," and the stock has returned 615.87% over the past year while AMD-watchers were arguing about market share slides. Custom Silicon Is Where Hyperscalers Are Spending Broadcom (NASDAQ:AVGO) reported AI semiconductor revenue of $8.40 billion last quarter, up 106% year over year, with management guiding $10.70 billion for next quarter and CEO Hock Tan targeting $100 billion in AI sales by 2027. Broadcom builds the custom accelerators and Ethernet AI switches hyperscalers actually deploy at scale. Marvell Technology (NASDAQ:MRVL) tells the same story from the design-partner side: data center revenue of $1.519 billion represented 73% of sales last quarter, custom AI design activity is at an all-time high with over 50 new opportunities across more than 10 customers, and management called the Celestial AI acquisition "transformational" for optical interconnect. The Lithography Monopoly Nobody Replaces ASML (NASDAQ:ASML) is the one name that collects a toll whether AMD, the GPU incumbent, or a hyperscaler's in-house design wins the AI chip war. Q1 revenue came in at $10.34 billion with a year-end backlog of $45.06 billion, and management raised the full-year outlook to a $42.47 billion to $47.19 billion range. The forward P/E sits at 39, with consensus analyst rating skewing strongly to buy (31 buys and 6 strong buys). CEO Christophe Fouquet noted demand for chips is outpacing supply and that customers are accelerating capacity plans. ASML holds an effective monopoly on EUV lithography. Every advanced AI chip on the planet, including AMD's, requires its equipment to exist. The AMD trade is fully discovered. The supplier stack remains under-owned. The picks-and-shovels names get paid no matter which logo ends up on the next data center accelerator, and they deserve a closer look than the GPU duopoly headline currently commands. The analyst who called NVIDIA in 2010 just named his top 10 AI stocks This analyst's 2025 picks are up 106% on average. He just named his top 10 stocks to buy in 2026. Get them here FREE.