Mortgage misery for millions: Borrowers face up to SIX interest rate hikes on Iran war inflation shock

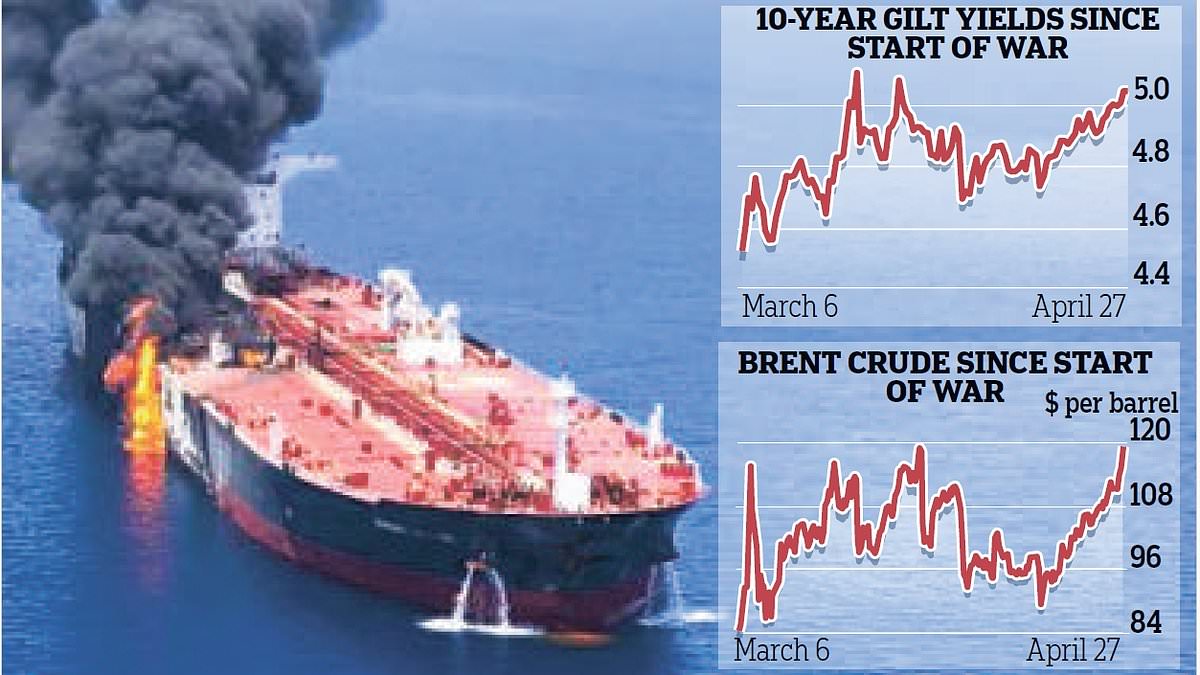

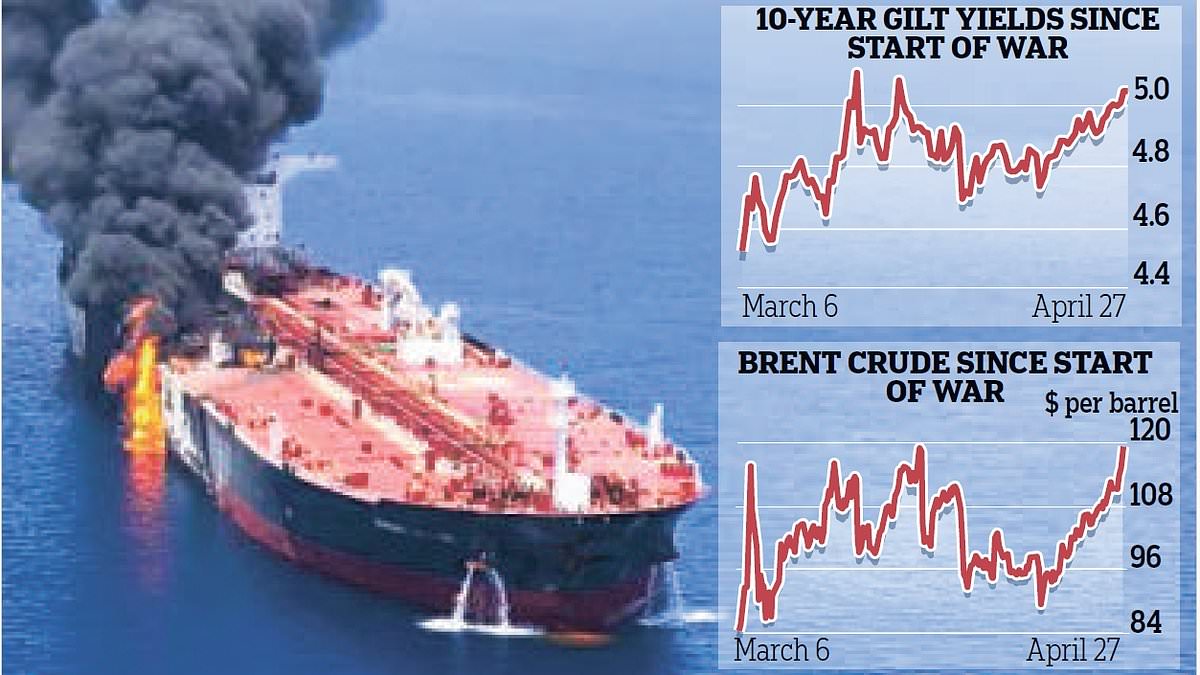

Borrowers could be battered with six interest hikes over the coming year if the Iran war causes a sustained rise in oil prices, the Bank of England has warned.The Bank’s Monetary Policy Committee (MPC) left rates on hold today but suggested a series of hikes to 5.25 per cent by the start of 2027 under a scenario where oil hits $130 a barrel.A rise in rates to 5.25 per cent ‘would raise the risk of a recession’, the Bank said. Brent crude spiked to $126 this morning before easing as fears grow that the conflict will continue to choke off energy supplies from the Middle East.Even under less severe scenarios in which the oil price starts to come down, the Bank signalled that it now looks almost certain to hike rates this year for the first time since 2023.The war has already pushed inflation to 3.3 per cent and could send it to 6.2 per cent in early 2027 under the adverse scenario modelled by the Bank.It could mean unemployment surging past two million to 5.7 per cent and economic growth slowing to a sluggish 0.8 per cent though the Bank is not predicting a recession – which is when the economy goes backwards for two quarters in a row.Even in less severe scenarios, inflation and unemployment rise and gross domestic product (GDP) growth weakens.

Bank of England governor Andrew Bailey is grappling with fallout from war in Middle EastFinancial markets are already expecting higher interest rates, which has fed through to higher mortgage costs – with monthly payments expected to rise by an average £80 a month according to the Bank.Members of the MPC will feel compelled to hike rates if they see inflation starting to spiral out of control.They remain in wait-and-see mode for now, voting to leave them on hold by 8-1. One member, chief economist Huw Pill, voted for a hike to 4 per cent.And even some of the more ‘dovish’ rate-setters – who tend to incline more towards cuts – indicated that rate hikes would be needed if the situation in the Middle East continues to deteriorate, some suggesting the Bank would have to act ‘forcefully if necessary’.Inflation is already rising thanks to higher petrol prices caused by the war, with a further spike likely when the energy price cap goes up in July.And the Bank expects that consumers will have to swallow the increases in the cost of living with price rises ‘likely to materialise more quickly’ than wages.Living standards are already falling with household income falling by 0.5 per cent in real terms in the current second quarter as prices shoot higher.Rate-setters will closely watch whether an inflation spike does turn into a wider spiral as workers demand higher pay.Bank of England governor Andrew Bailey said: ‘The war in the Middle East is causing inflation to rise again this year.‘We’ve held Bank rate unchanged at 3.75 per cent.‘We think this is a reasonable place given the situation of the economy and the unpredictability of events in the Middle East.‘We’ll continue to monitor the situation and its impact on the UK economy very closely.‘Whatever happens, our job is to make sure that inflation gets back to the 2 per cent target after the initial impact of the war on energy prices has passed.’Ed Monk, a pensions and investment specialist at Fidelity International, said today’s decision ‘may be the calm before the storm’.And he warned that a series of rate hikes in the coming months ‘would place a hard brake on an economy that is forecast to grow only slightly this year’.Martin Beck, chief economist at WPI Strategy, said: ‘Today’s Bank of England decision underlines a Monetary Policy Committee grappling with an unusually uncertain outlook.‘At the heart of the debate is how persistent the recent rise in energy prices will prove, and whether its impact on inflation fades or becomes more embedded.‘Faced with that uncertainty, the MPC has opted for the least risky course: to wait.’Professor Joe Nellis, an economic adviser at accountancy firm MHA, said: ‘The long-term picture of the UK economy is still uncertain, but it is becoming clearer that weak growth, coupled with rising inflation pressure, will be a defining characteristic.’How to find a new mortgage Mortgage rates have soared after conflict with Iran has driven up inflation expectations and dashed hopes of interest rate cuts.If you need a mortgage because you are buying a home, or your current fixed rate deal is due to end, you should explore your options as soon as possible. This is Money has a long-standing partnership with fee-free broker L&C, to provide you with expert mortgage advice.Use This is Money and L&Cs best mortgage rates calculator to show deals matching your home value, mortgage size, term and fixed rate needs.Or use L&C’s online Mortgage Finder to search thousands of deals from more than 90 different lenders to discover the best deal for you.This is Money's mortgage tips What if I need to remortgage? Borrowers should compare rates, speak to a mortgage broker and be prepared to act. Homeowners can lock in to a new deal six to nine months in advance, often with no obligation to take it.Most mortgage deals allow fees to be added to the loan and only be charged when it is taken out. This means borrowers can secure a rate without paying arrangement fees. If you do this and don't clear the fee on completion, interest will be paid on it over the term of the loan.What if I am buying a home? Those with home purchases agreed should also aim to secure rates as soon as possible, so they know exactly what their monthly payments will be. Buyers should avoid overstretching and be aware that house prices may fall, as higher mortgage rates limit people's borrowing ability and buying power.What about buy-to-let landlords?Buy-to-let landlords with interest-only mortgages will see a greater jump in monthly costs than homeowners on residential mortgages. This makes remortgaging in plenty of time essential and our partner L&C can help with buy-to-let mortgages too. > Find your next mortgage deal with This is Money and L&CMortgage service provided by London & Country Mortgages (L&C), which is authorised and regulated by the Financial Conduct Authority (registered number: 143002). The FCA does not regulate most Buy to Let mortgages. Your home or property may be repossessed if you do not keep up repayments on your mortgage